Journal of Resources and Ecology >

The Framework of the Natural Resources Report—Improvements based on the Natural Resource Accounting Administration Demands of China

Received date: 2023-05-08

Accepted date: 2023-08-06

Online published: 2023-12-27

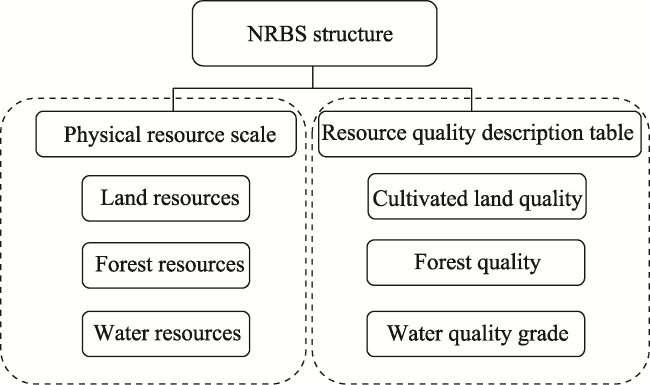

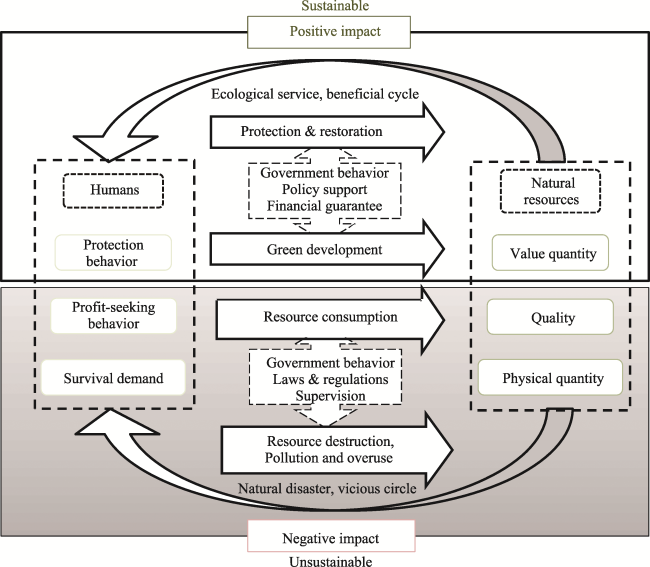

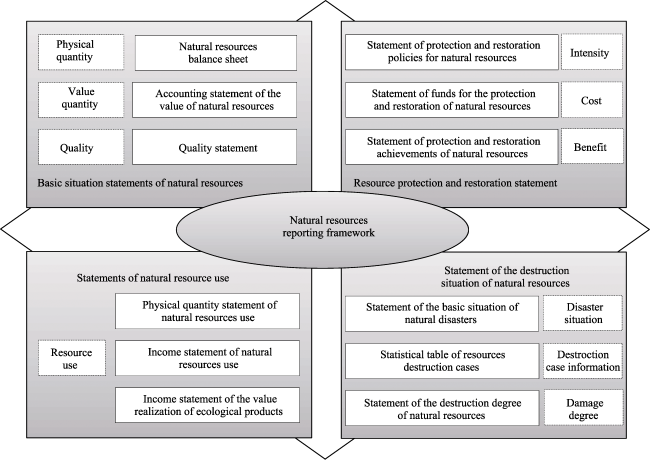

Based on the existing research on natural resource accounting, this study attempts to further enrich the administrative attributes of natural resource accounting. Through the analysis and comparison of previous publications, a mechanism for improving the construction of the natural resources report is proposed, with the dual aims of meeting the Chinese government’s supervision and audit demands in resource administration and overcoming the deficiencies of the Natural Resources Balance Sheet (NRBS) in scientific research and actual practice. By analyzing the influences of human factors on natural resources, the information structure and accounting contents of the natural resources report are given. The results demonstrate that the natural resource report system is reasonable and feasible in terms of its logical and theoretical basis. The framework of the system consists of four parts: the statement of the basic situation of natural resources, the statement of the protection and restoration of natural resources, the statement of resource use, and the statement of the degree of destruction of the natural resources. The results of this study provide reference statements for the NRBS, the natural resource quality statement, the protection and restoration policy statement, the protection and restoration funding statement, the natural disaster statement, and the registration form of resource destruction cases. This study provides a reference for the innovation of the natural resource administration system, in which the supervision and administration of natural resources are the main criteria.

ZHANG Xinye , CHEN Yaru , ZHANG Ning , SONG Boyao , MA Shangyu . The Framework of the Natural Resources Report—Improvements based on the Natural Resource Accounting Administration Demands of China[J]. Journal of Resources and Ecology, 2024 , 15(1) : 227 -241 . DOI: 10.5814/j.issn.1674-764x.2024.01.020

Table 1 Natural resource balance sheet (land) (Unit: ha) |

| Assets | Value | Liabilities | Value |

|---|---|---|---|

| Cultivated land | Construction occupation | ||

| Garden land | Disaster destruction | ||

| Forest land | Illegal occupation | ||

| Grassland | Everything else | ||

| Urban village and industrial land | |||

| Transport land | Net assets | ||

| Waters and water conservancy facility land | Cultivated land | ||

| Other land | Garden land | ||

| Forest land | |||

| Liability offset | Grassland | ||

| Comprehensive land management | Urban village and industrial land | ||

| Agricultural structural adjustment | Transport land | ||

| Cropland conversion | Waters and water conservancy facility land | ||

| Everything else | Other land | ||

| Total |

Note: The totals for the second and fourth columns are equal. The table is designed for the account of natural resource information statistics, thus some fields remain unpopulated. The same below. |

Table 2 Natural resource balance sheet (forest) (Unit: 103 m3) |

| Assets | Value | Liabilities | Value |

|---|---|---|---|

| Natural forest | Logging | ||

| Non-commercial forest | Deforestation | ||

| Commercial forest | Disaster losses | ||

| Planted forest | Natural reductions | ||

| Non-commercial forest | Everything else | ||

| Commercial forest | Net assets | ||

| Bamboo grove | Natural forest | ||

| Non-commercial forest | |||

| Liability offset | Commercial forest | ||

| Forestation | Planted forest | ||

| Grain for green | Non-commercial forest | ||

| Natural growth | Commercial forest | ||

| Everything else | Bamboo grove | ||

| Total |

Table 3 Natural resource balance sheet (water resources) (Unit: 104 m3) |

| Assets | Value | Liabilities | Value |

|---|---|---|---|

| Surface water | Water intake | ||

| Reservoirs | Living water | ||

| Lakes | Industrial water | ||

| Rivers | Agricultural water | ||

| Ground water | Off-river ecological water | ||

| Flow out | |||

| Liability offset | Flow outside the area | ||

| Inflow of water resources formed by precipitation | Flow to the sea | ||

| Inflow from outside the area | Call out of the area | ||

| Call in from outside the region | Ecological water consumption of rivers and lakes | ||

| Inflow from other water sources in the region | |||

| Return amount of economic and social water | Net assets | ||

| Return amount of irrigation water | Surface water | ||

| Amount of waste water entering the river | Reservoirs | ||

| River inflow after treatment | Lakes | ||

| Rivers | |||

| Ground water | |||

| Total |

Table 4 The quality of forest resources (Unit: 103 m3) |

| Quality evaluation indicator | Opening balance | Increase | Decrease | Ending balance |

|---|---|---|---|---|

| Stock per unit area of planted forest | ||||

| Stock per unit area of natural forest | ||||

| Total |

Table 5 The quality of water resources |

| Quality evaluation indicators | Reservoirs | Lakes | Rivers | Underground water | ||||

|---|---|---|---|---|---|---|---|---|

| Opening | Ending | Opening | Ending | Opening | Ending | Opening | Ending | |

| ClassⅠ | ||||||||

| Class Ⅱ | ||||||||

| Class Ⅲ | ||||||||

| Class Ⅳ | ||||||||

| Class Ⅴ | ||||||||

| Lower Class Ⅴ | ||||||||

Table 6 The quality of grassland resources |

| Quality evaluation indicator | Opening balance | Increase | Decrease | Ending balance |

|---|---|---|---|---|

| Grassland vegetation types | ||||

| Grassland vegetation height | ||||

| Grassland vegetation coverage | ||||

| Aboveground biomass |

Table 7 Statement of the protection and restoration policies for natural resources |

| Resource category | Policy name | Policy release department | Date of issue | Policy category | Subsidy standard | Source of funds | Way of using funds |

|---|---|---|---|---|---|---|---|

| Land resources | |||||||

| Water resources | |||||||

| Forest resources | |||||||

| Everything else (Grassland resources etc.) |

Table 8 Statement of funds for the protection and restoration of natural resources |

| Resource category | Year | Total | Fund name A Quota Source | Fund name B Quota Source | …… |

Table 9 Statement of protection and restoration achievements related to natural resources |

| Protection and restoration project | Changes in resources | Changes in resource quality |

|---|---|---|

| Opening balance Increase Closing balance | Opening balance Closing balance |

Table 10 Physical scale of natural resource utilization |

| Resource category | Utilization mode | Unit | Utilization of physical quantity |

|---|---|---|---|

| Land resources | Agricultural land | ||

| Industrial land | |||

| Forest resources | Timber | ||

| Freshwater resources | Drinking water | ||

| Industrial water | |||

| Grassland resources | |||

| …… | |||

| Mineral resources | |||

| …… |

Filling time: yyyy-mm-dd -yyyy-mm-dd. |

Table 11 Income statement of natural resources use |

| Resource category | Product name | Unit | Quantity | Unit price | Revenue | Operating costs | Profit |

|---|---|---|---|---|---|---|---|

| Land resources | Compensated use | ha | |||||

| Forest resources | Timber | m3 | |||||

| Grassland resources | Feed | ||||||

| …… | |||||||

| Mineral resources | Coal mine | t |

Filling time: yyyy-mm-dd -yyyy-mm-dd. |

Table 12 Income statement of the value realization of ecological products |

| Resource category | Green product name | Quantity | Unit Price | Revenue | Operating costs | Profit |

|---|---|---|---|---|---|---|

| Land resources | ||||||

| Forest resources | Forest health | |||||

| Understory economy | ||||||

| Grassland resources | Ecotourism | |||||

| Mineral resources | ||||||

| …… |

Filling time: yyyy-mm-dd -yyyy-mm-dd. |

Table 13 Statement of the basic situation of natural disasters |

| Major disaster | Disaster type | Time of occurrence | Place of occurrence | Cause | Types of resources involved |

Table 14 Statistical table of resource destruction cases |

| Year | Resource type | Number of cases | Specific destructive behavior | How the situation was managed |

Table 15 Statement of the degree of destruction of natural resources |

| Resource destruction event type | Changes in resources | Changes in resource quality |

|---|---|---|

| Before occurrence Reduced/destroyed after occurrence | Before occurrence After occurrence |

| [1] |

|

| [2] |

|

| [3] |

|

| [4] |

|

| [5] |

|

| [6] |

|

| [7] |

|

| [8] |

|

| [9] |

|

| [10] |

|

| [11] |

|

| [12] |

|

| [13] |

|

| [14] |

|

| [15] |

|

| [16] |

|

| [17] |

|

| [18] |

|

| [19] |

|

| [20] |

|

| [21] |

|

| [22] |

|

| [23] |

|

| [24] |

|

| [25] |

|

| [26] |

|

| [27] |

|

| [28] |

|

| [29] |

|

| [30] |

|

| [31] |

|

| [32] |

|

| [33] |

|

| [34] |

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}