Journal of Resources and Ecology >

Supply and Demand Levels for Livestock and Poultry Products in the Chinese Mainland and the Potential Demand for Feed Grains

Received date: 2020-01-15

Accepted date: 2020-05-25

Online published: 2020-09-30

Supported by

The Key Deployment Project of Chinese Academy of Sciences(ZDBS-SSW-DQC)

The widening gap between the supply and demand levels for livestock and poultry products in the Chinese mainland poses a significant challenge to the secure supply of feed grains. Therefore, the accurate prediction of the demand potential for feed grains represents a key scientific issue for ensuring food security in the Chinese mainland. This study is based on an analysis of several factors, such as the Chinese mainland’s output, trade volume, apparent consumption of livestock and poultry products, and two different scenarios for predicting the future demand for feed grains are assessed. The results indicate that output and consumption of livestock and poultry products, as well as the country’s trade deficit and the pressure of the supply and demand balance with respect to these products, have been increasing in recent years. The analysis predicts that the demand for feed grains in the Chinese mainland will reach 425.5 or 389.6 million tons in 2030 based on the two scenarios. This finding indicates that with the increasing demand for livestock and poultry products in the Chinese mainland, the demand for feed grains will continue to increase, and the shortfall in feed grains and raw materials will expand further, especially dependence on external sources of protein-rich feed grains will remain high.

HUANG Shaolin , LIU Aimin , LU Chunxia , MA Beibei . Supply and Demand Levels for Livestock and Poultry Products in the Chinese Mainland and the Potential Demand for Feed Grains[J]. Journal of Resources and Ecology, 2020 , 11(5) : 475 -482 . DOI: 10.5814/j.issn.1674-764x.2020.05.005

Table 1 Parameters relevant to the measurement and calculation of feed grains |

| Category | Feed-to-meat (eggs) conversion ratio | Dressing percentage (%) | Energy feed ratio (%) | Protein feed ratio (%) |

|---|---|---|---|---|

| Pork | 2.8 | 70 | 73 | 22 |

| Poultry meats | 2.0 | 76 | 73 | 22 |

| Poultry eggs | 2.4 | 100 | 73 | 22 |

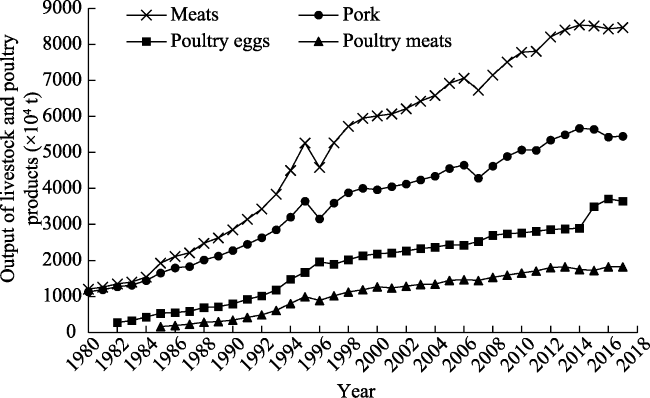

Fig. 1 Changes in the output of the main livestock and poultry products (Data source: FAOSTAT, 1980-2017) |

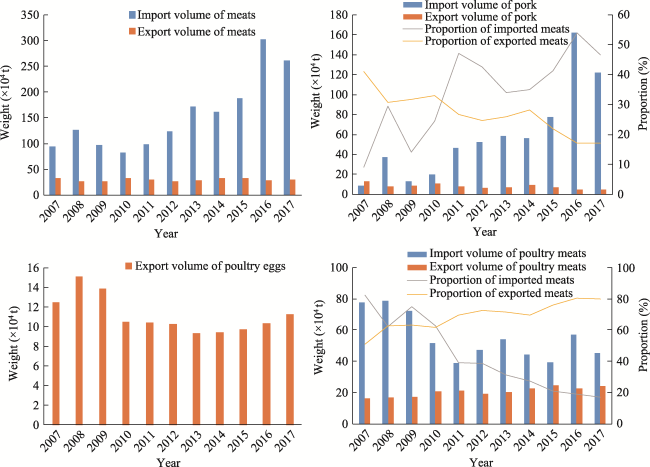

Fig. 2 Changes in the trade volume of the Chinese mainland’s livestock and poultry products (Data source: FAOSTAT, 2007—2017) |

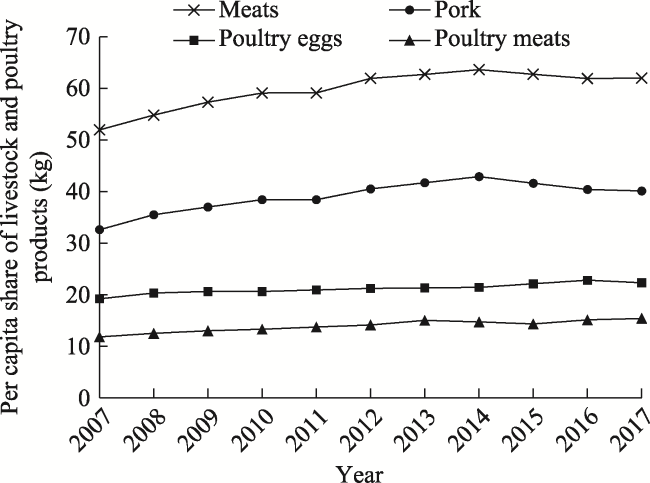

Fig. 3 Changes in the per capita share of livestock and poultry products in the Chinese mainland in the past decade |

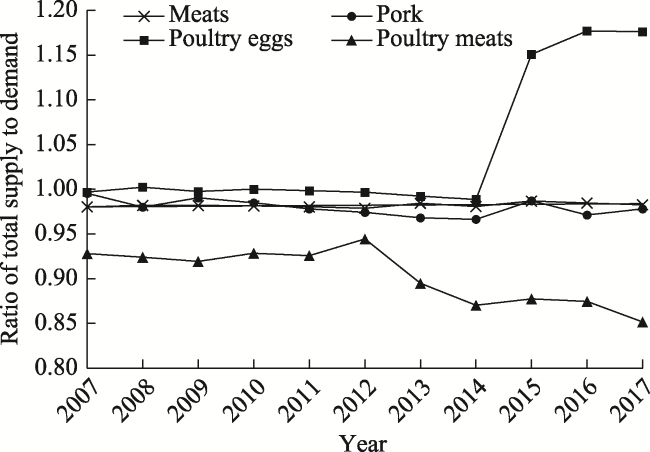

Fig. 4 Ratio of total supply to demand for the Chinese mainland’s livestock and poultry products in the last decade |

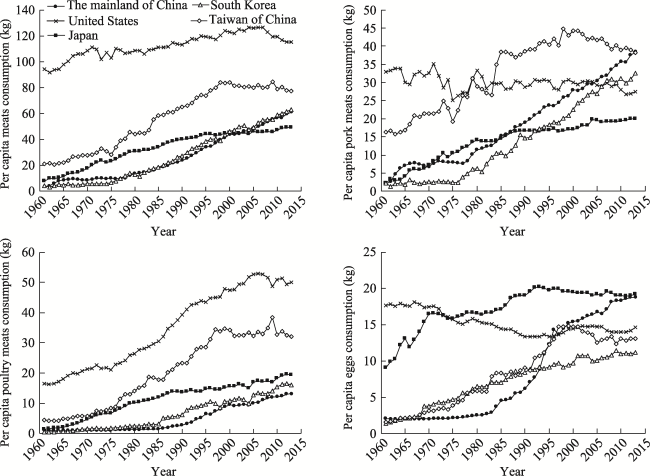

Fig. 5 Comparisons of per capita apparent consumption of livestock and poultry products (Data source: FAOSTAT, 1961-2013) |

Table 2 Current demand for feed grains |

| Category | Per capita share (kg) | Total share (×104 t) | Demand for energy feed grains (×104 t) | Demand for protein feed grains (×104 t) |

|---|---|---|---|---|

| Pork | 40.1 | 5574.2 | 16276.7 | 4905.3 |

| Poultry meats | 15.4 | 2140.7 | 4112.4 | 1239.4 |

| Poultry eggs | 22.3 | 3099.9 | 5431.0 | 1636.7 |

| Total | 77.8 | 10814.8 | 25820.2 | 7781.4 |

Table 3 Future demands for feed grains in different scenarios |

| Scenarios | Category | Per capita share (kg) | Total share (×104 t) | Demand for energy feed grains (×104 t) | Demand for protein feed grains (×104 t) |

|---|---|---|---|---|---|

| Taiwan region’s consumption of livestock and poultry products | Pork | 47.5 | 6887.5 | 20111.5 | 6061.0 |

| Poultry meats | 24.2 | 3509.0 | 7318.8 | 2205.7 | |

| Poultry eggs | 23.0 | 3335.0 | 5842.9 | 1760.9 | |

| Total | 94.7 | 13731.5 | 33273.2 | 10027.5 | |

| Nutritional intake target | Pork | 43.7 | 6333.5 | 18493.7 | 5573.4 |

| Poultry meats | 20.1 | 2916.0 | 5601.7 | 1688.2 | |

| Poultry eggs | 23.0 | 3355.0 | 5842.9 | 1760.9 | |

| Total | 86.8 | 12584.4 | 29938.3 | 9022.5 |

Note: Among the first scenario, the pork and poultry meat consumption structures are calculated according to the predictions of Cheng et al. (2016). |

| 1 |

|

| 2 |

|

| 3 |

|

| 4 |

General Office of the State Council. 2014. Outline of China’s food and nutrition development (2014-2020). Beijing: People’s Publishing House. (in Chinese)

|

| 5 |

General Office of the State Council. 2016. National population development plan(2016-2030).2016. National population development plan (2016-2030).http://www.gov.cn/zhengce/content/2017-01/25/content_5163309.htm . Viewed 25 Jan. 2017.

|

| 6 |

|

| 7 |

|

| 8 |

|

| 9 |

|

| 10 |

|

| 11 |

|

| 12 |

|

| 13 |

|

| 14 |

|

| 15 |

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}