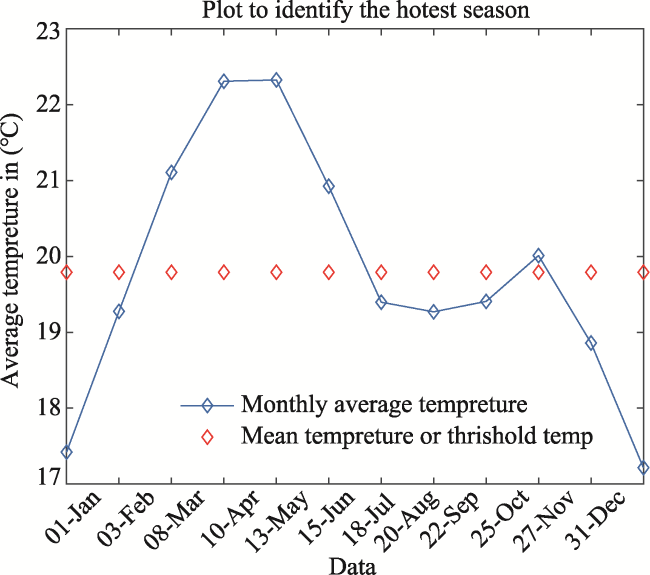

In this paper we model the dynamics of temperature using Ornstein-Uhlenbeck process approach and then we calculate the price of weather derivative based on different temperature indices. We know that the payoff temperature contract depends on the cumulative temperature indices over the contract period. So, to calculate reasonable pricefor different type of temperature contract like future and option, we need to have a model that accurately characterizes the dynamics of temperature. When we develop a mathematical model describing temperature movements, the basic features of temperature such as trend due to green house and urbanization, seasonality of mean temperature, autoregressive properties for temperature changes, and seasonal variations in volatility should be taken into consideration in order to get precise model. In the last two decades several researches have been conducted for studying temperature processes, constructing and pricing weather derivatives written on temperature.

Dornier and Querel (2000) suggested Ornstein-Uhlenbeck (OU) process to model Chicago temperature data and the volatility has been considered as a constant.

Alaton et al. (2002) applied the Ornstein-Uhlenbeck process to model temperature data the Stockholm, Sweden. The volatility of the temperature process varies through different months and it has been modeled as a piece-wise function with constant value each month. They price different temperature indices based on the resulting model.

Zhu et al. (2012) used the same model as Alaton P’ model (

Alaton et al., 2002) for modelling daily temperature in a dry region of China in order to price drought option through stochastic simulation. (

Mraoua and Bari, 2007) presented a price model for weather derivatives with payouts depending on temperature indices. They have used a mean-reverting stochastic process to characterize dynamics of the temperature data recorded for 44 years on the area of Casablanca, Morocco. Their model is easily tractable to simulate a temperature swap contract.

Fred E. Benth and Saltyte-Benth (2005) suggested a mean- reverting Ornstein-Uhlenbeck process driven by generalized hyperbolic Levy process and having seasonal mean and volatility to model the daily average temperature variations.

Benth and Saltyte-Benth (2007) proposed Ornstein-Uhlenbeck process with seasonal volatility to model the time dynamics of daily average temperature for Stockholm. They used a truncated Fourier series to model the seasonal volatility, and validate their model on more than 40 years of daily data collected from Stockholm, Sweden. They also provide explicit formulas for options written on heating, cooling degree-days and cumulative average temperature (CAT) futures.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}